Discount and convenience stores in the U.S. are projected to grow faster than all other offline retail channels over the next five years.

This projected growth reflects consumers' increased focus on price and speed, even if that means a more limited assortment, according to an analysis from e-commerce insights company Edge by Ascential.

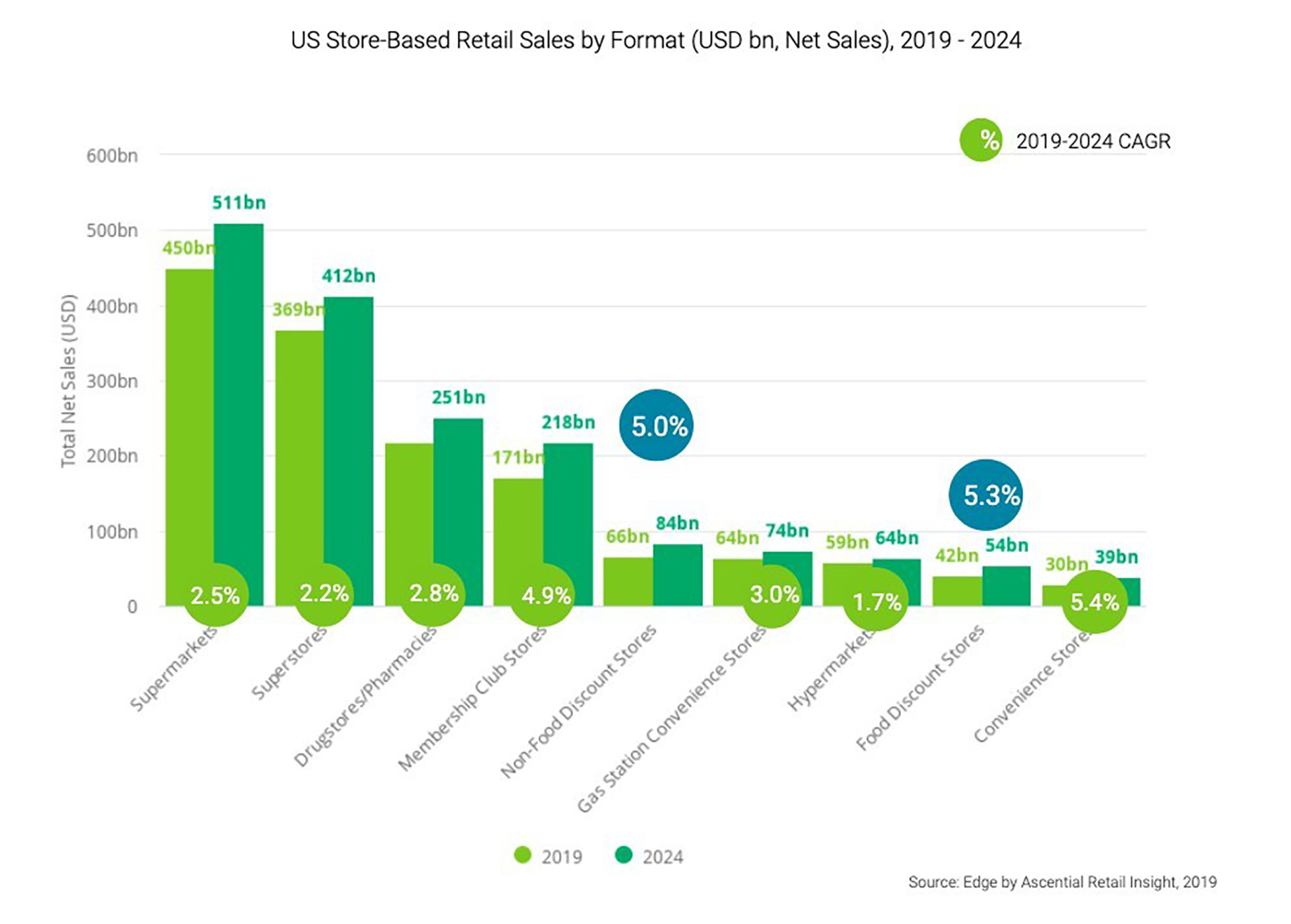

The firm is projecting that nonfood discount, food discount and convenience stores will all grow at annual rates above 5 percent, versus 3 percent or below for all other offline retailers, aside from membership-club stores. The firm anticipates that convenience stores will have the highest growth rate, at 5.4 percent, with discount and nonfood discount stores growing at 5.3 percent and 5 percent, respectively.

The forecast seems to reflect broader economic trends, observes David Gordon, research director at Edge by Ascential. "What we're seeing offline is similar to what we're seeing online," he said in a press release. "There's an increasing emphasis on low cost and convenience. You can see it through the lens of Amazon, and it will continue to play out online in similar ways."

U.S. projections largely reflect what is projected on a global scale, where convenience stores (at 6.6 percent growth), nonfood discount stores (5.2 percent) and discount stores (4.9 percent) join membership-club stores in experiencing the fastest growth.

This growth can be manifested in the chains that were planning to add U.S. stores in 2019, says Gordon. German-owned discounter Aldi, for one, was expected to open about 100 stores. Roughly 1,000 Dollar General stores were anticipated to open, with hundreds of those set to add produce and fresh foods to their offering. Observers were looking for a net increase of about 160 Dollar Tree and Family Dollar stores, as well.

Expectations are for roughly 1,000 new Dollar General stores by year-end 2019

Projections are that food discount stores, in particular, will keep gaining overall share, increasing to 9.7 percent of food sales in 2024, up from 8.8 percent today and 7.4 percent in 2014, according to the firm's research.

Convenience stores will continue to thrive, thanks to urbanization, declining household sizes and a preference for smaller shopping missions, according to Gordon. They are also proving to be relatively resistant to share losses from online retailers — a mere 0.2 percent loss in share between 2013 and 2018, he cites.

Discount stores, too, are seeking to "future-proof" their market share, Gordon says. Many of them are forming partnerships with online delivery intermediaries, which help support a last-mile solution that fits the lower-cost, low-complexity discount model.

By Brannon Boswell

Executive Editor, Commerce + Communities Today